Bridging loans for auction properties are one of the most practical tools available to UK property buyers. When the hammer falls, you have very little time — and traditional mortgage finance simply cannot keep up with auction deadlines.

This guide explains how auction property finance works in practice, why bridging loans for auction properties are the go-to solution for buyers at every level, what the legal process involves, and how a specialist bridging loan solicitor keeps your transaction on track when time is against you.

Why bridging loans for auction properties are the standard solution

Property auctions operate on a strict timetable. The moment your bid is accepted, a legally binding contract is created. You are typically required to pay a 10% deposit immediately and complete the purchase — paying the remaining 90% — within 28 days.

Standard residential mortgages usually take four to eight weeks to arrange, even in straightforward cases. They also require the property to meet strict habitability criteria that many auction lots simply do not satisfy.

Bridging loans for auction properties solve both problems at once. They can be arranged in days rather than weeks, they are secured against the property itself rather than tied to your income, and lenders assess each case individually — meaning properties in poor condition or with unusual characteristics are often still fundable.

For a direct comparison of your financing options before bidding, our guide on whether to use a mortgage or bridging loan for your auction purchase sets out the key differences clearly, including when each option is the right fit.

How auction property finance actually works

Understanding the mechanics of auction finance before you attend is essential. Many buyers arrive at auctions without finance confirmed and find themselves either unable to bid confidently or scrambling to meet the deadline after winning.

Before the auction

Ideally, arrange your auction property finance before you set foot in the room — or place a bid online. Most bridging lenders can issue a Decision in Principle within 24 to 48 hours once they understand the property, the amount required, and your exit strategy. Having this in place lets you bid with confidence, knowing the funds are available if you win.

On auction day

When your bid is accepted, you sign the contract and pay the deposit — typically 10% of the purchase price — immediately. There is no cooling-off period. From this point, the 28-day completion clock starts. Failing to complete means losing your deposit and potentially facing further legal liability.

Between exchange and completion

This is the critical window for bridging loans for auction properties. Your lender will instruct a valuation, and your solicitor will work through the legal title, carry out any necessary property searches, and prepare the completion documentation. The speed and quality of your legal team during this period is often what determines whether you meet the deadline comfortably or under pressure.

At completion

On the completion date, the bridging lender releases funds to your solicitor, who transfers the balance to the seller’s solicitors. Your auction property finance is drawn down, the title is transferred to you, and any necessary charge is registered at the Land Registry. You now own the property.

What a bridging loan solicitor does in an auction transaction

A bridging loan solicitor plays a central and time-critical role in every auction purchase funded by bridging finance. Their work runs in parallel with the lender’s process and must be completed within the same tight timeframe.

The legal work a bridging loan solicitor handles typically includes:

- Reviewing the auction legal pack on your behalf before you bid — identifying title issues, unusual conditions, or risks that could affect the loan or the purchase

- Conducting property searches, including local authority, drainage, and environmental checks, which lenders require before releasing funds

- Reviewing and advising you on the loan agreement, ensuring you understand the interest structure, fees, and repayment obligations before signing

- Registering the lender’s legal charge against the property at the Land Registry

- Managing the secure transfer of completion funds between lender, buyer, and seller

- Advising on your exit strategy and any implications for the legal title once the loan is repaid

Instructing an experienced bridging loan solicitor early — ideally before the auction — significantly reduces the risk of delays at the legal stage. A solicitor who specialises in this area will be familiar with lenders’ documentation requirements and will know how to progress the file efficiently when time is limited.

You can find out more about how our team works and what to expect from the legal process on the how it works section of our website. We outline each stage clearly, from initial consultation through to loan completion.

Types of properties suited to bridging loans for auction

One of the significant advantages of bridging loans for auction properties is the flexibility of what can be funded. Traditional mortgage lenders often decline properties that fall outside standard habitability criteria. Bridging lenders take a different view, making this type of finance particularly well-suited to the kinds of properties commonly sold at auction.

Properties typically funded through auction bridging finance include:

- Uninhabitable or unmortgageable properties: Properties lacking a working kitchen, bathroom, or heating system are routinely declined by mortgage lenders. Bridging lenders assess the property’s value and your renovation plans instead.

- Properties requiring major renovation: Buyers planning to refurbish before refinancing or selling can often include renovation costs within the bridging loan, depending on the lender and the scale of work.

- Properties with title complications: Short leases, missing planning permissions, or unusual covenants can delay or prevent a mortgage. Bridging finance can provide short-term funding while these issues are resolved.

- Commercial and mixed-use properties: Auction finance is not limited to residential purchases. Shops, offices, HMOs, and mixed-use buildings are all regularly funded through short-term bridging products.

- Land with or without planning permission: Bridging finance can fund land purchases, including sites awaiting planning approval or subject to development conditions that standard lenders will not consider.

Planning to buy at a property auction?

Before bidding, a bridging loan solicitor can review the auction legal pack, check title issues, and confirm the property is suitable for bridging finance. Get advice

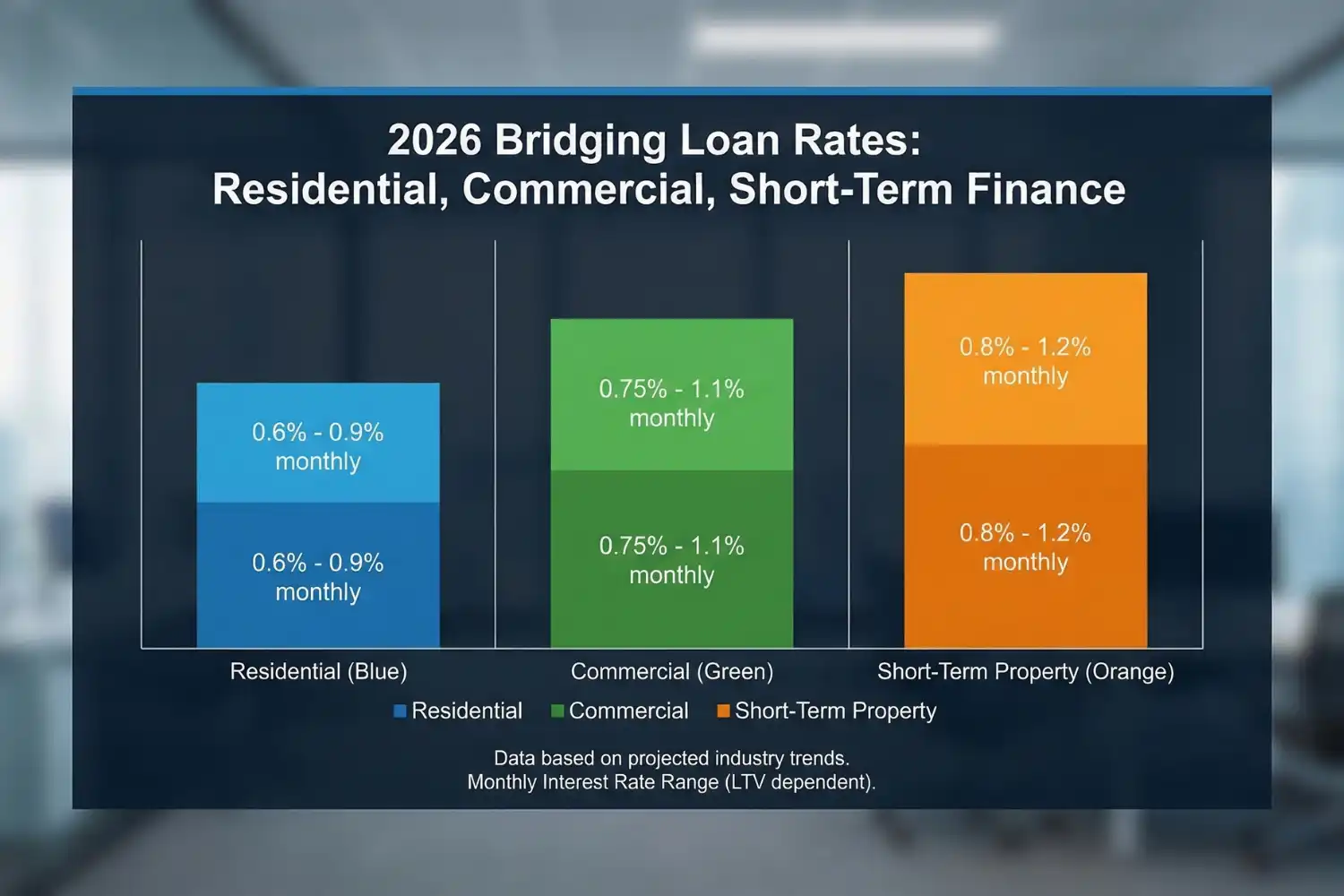

Costs and terms: what to expect

Auction property finance is not cheap compared to a standard mortgage. The cost reflects the speed, flexibility, and risk the lender accepts. Understanding what you will pay — and when — is essential before you bid.

Typical costs associated with a bridging loan for an auction purchase include:

- Monthly interest: Bridging loans charge interest monthly rather than annually. Rates typically range from 0.5% to 1.5% per month depending on the lender, loan size, LTV, and your exit strategy.

- Arrangement fee: Most lenders charge 1–2% of the loan amount as an arrangement fee, usually added to the loan rather than paid upfront.

- Valuation fee: The lender will require a professional valuation of the property before releasing funds. This is typically paid upfront and ranges from a few hundred to over a thousand pounds depending on the property type.

- Legal fees: You will pay your own solicitor’s fees for the conveyancing work, and in many cases you may also be required to contribute towards the lender’s legal costs.

- Exit fees: Some lenders charge a fee on repayment, though many do not. Always confirm this before agreeing terms, particularly if you anticipate repaying early.

The total cost of bridging loans for auction properties depends significantly on how long you hold the loan. Because interest accrues daily or monthly, repaying as quickly as possible — once your exit plan is achieved — always saves money. Most bridging loans run for between one month and 18 months.

Exit strategies: the foundation of every bridging loan for auction properties

No lender will offer bridging loans for auction properties without a clear and credible exit strategy. The exit strategy is your plan for repaying the loan — and lenders assess it as carefully as they assess the property itself.

The most common exit strategies used in auction bridging transactions are:

- Refinancing onto a standard mortgage: Once the property meets mortgageability criteria — typically after renovation or after resolving title issues — the bridging loan is repaid by switching to a residential or buy-to-let mortgage.

- Sale of the property: Investors buying at a discount, or developers planning to refurbish and sell, will repay the bridging loan from the sale proceeds. The loan must be repayable within the expected sale timeline.

- Sale of another asset: If you have tied-up equity in an existing property, the proceeds from that sale can form your exit. This is common where a buyer’s current home is on the market but has not yet completed.

- Development refinance: For larger development projects, the exit may be to a specialist development finance product rather than a standard mortgage, based on the gross development value of the completed scheme.

Your solicitor plays an important role here too. Bridging loan solicitors can identify at an early stage whether your proposed exit is legally achievable — for example, whether a property is likely to be mortgageable after the planned works — and alert you to any title issues that could delay or prevent refinancing.

How quickly can bridging finance be arranged for an auction?

Speed is the defining characteristic of auction property finance, and experienced lenders and solicitors are structured to deliver it. In straightforward cases, bridging finance can complete within five to ten working days. More complex transactions — unusual property types, title complications, or larger loan sizes — typically take two to three weeks.

For bridging loans for auction properties, the practical minimum is usually around five working days, assuming the legal pack is clean, the valuation can be arranged quickly, and all parties respond promptly. Ultra-fast completions within 48 to 72 hours are possible in rare circumstances but should not be relied upon as a planning assumption.

Our dedicated article on bridging loan speed in the UK goes into the detail on what affects completion timelines, the stages where delays most commonly occur, and how to structure your transaction to move as quickly as possible within the 28-day window.

Key risks to understand before using bridging loans for auction properties

Bridging finance is not without risk, and buyers who use it without a clear plan can find themselves in serious financial difficulty. Understanding the main risks before you bid is a fundamental part of responsible auction buying.

- Failing to repay within the term: If your exit strategy fails — the refinancing falls through, the property does not sell, or the works take longer than planned — you may face default interest, penalty charges, or enforcement action by the lender.

- Property value shortfall: Bridging loans are secured against the property. If the property’s value falls below expectations — or the lender’s valuation comes in lower than your bid — you may not be able to borrow as much as you need.

- Auction legal pack issues: Many auction properties are sold with complex or incomplete legal packs. Issues discovered after you have bid — such as missing planning permissions, unresolved charges, or adverse covenants — can delay or complicate the transaction significantly.

- Underestimating renovation costs: If your exit depends on selling a refurbished property or refinancing after works, cost overruns can erode the margin on which your plan is based and put repayment in jeopardy.

Having a bridging loan solicitor review the auction legal pack before you bid is one of the most effective ways to reduce these risks. They can identify issues that are not immediately obvious to a non-specialist — and advise you on whether those issues are manageable within your timeline and budget, or whether they make the property unsuitable for the finance you have in mind.

Getting the legal side right: how Bridging Loan Lawyers can help

Bridging loans for auction properties require solicitors who understand both the time pressures of auction transactions and the specific legal requirements of short-term secured lending. A general conveyancer without this experience can slow a transaction down significantly — or miss issues that a specialist would catch before they become problems.

At Bridging Loan Lawyers, our bridging loan solicitors act exclusively for borrowers in short-term, development, and commercial loan transactions. We are structured for speed, we respond to enquiries within two hours, and we know exactly what lenders require at every stage of the process.

If you are planning to buy at auction and want to understand the legal process, costs, or timing for your specific situation, you are welcome to get in touch with our team directly. You can also read more about who we are and how we work before getting in touch — we offer a free, no-obligation initial consultation to all new clients.

The auction room moves fast. Having the right legal support in place before the hammer falls is what separates a smooth transaction from a stressful one.

Buying an auction property with a bridging loan?

When the hammer falls, you usually have just 28 days to complete. A specialist bridging loan solicitor can review the auction legal pack, advise on the loan agreement, and help ensure your auction property finance completes on time.