The deposit for a bridging loan is typically between 25% and 40% of the property’s value, depending on the lender, the type of loan, and the risk profile of your transaction. In bridging finance, this is usually expressed as loan-to-value (LTV) rather than a straight deposit figure — most lenders work to a maximum LTV of 70%–75%, which means you need to cover the remaining 25%–30% yourself.

Importantly, your “deposit” does not always have to be cash in the bank. Equity in another property, or in some cases other high-value assets, can count towards the security that lenders require. This makes bridging finance particularly useful for property investors and developers who have capital tied up in existing assets rather than sitting in a current account.

This guide explains how bridging loan deposit requirements work in practice, what affects the amount you need, and how to potentially reduce the deposit you put in.

What is loan-to-value and why does it matter for bridging?

Before diving into deposit figures, it helps to understand bridging loan LTV — the concept that sits at the heart of how bridging lenders assess how much they will lend you.

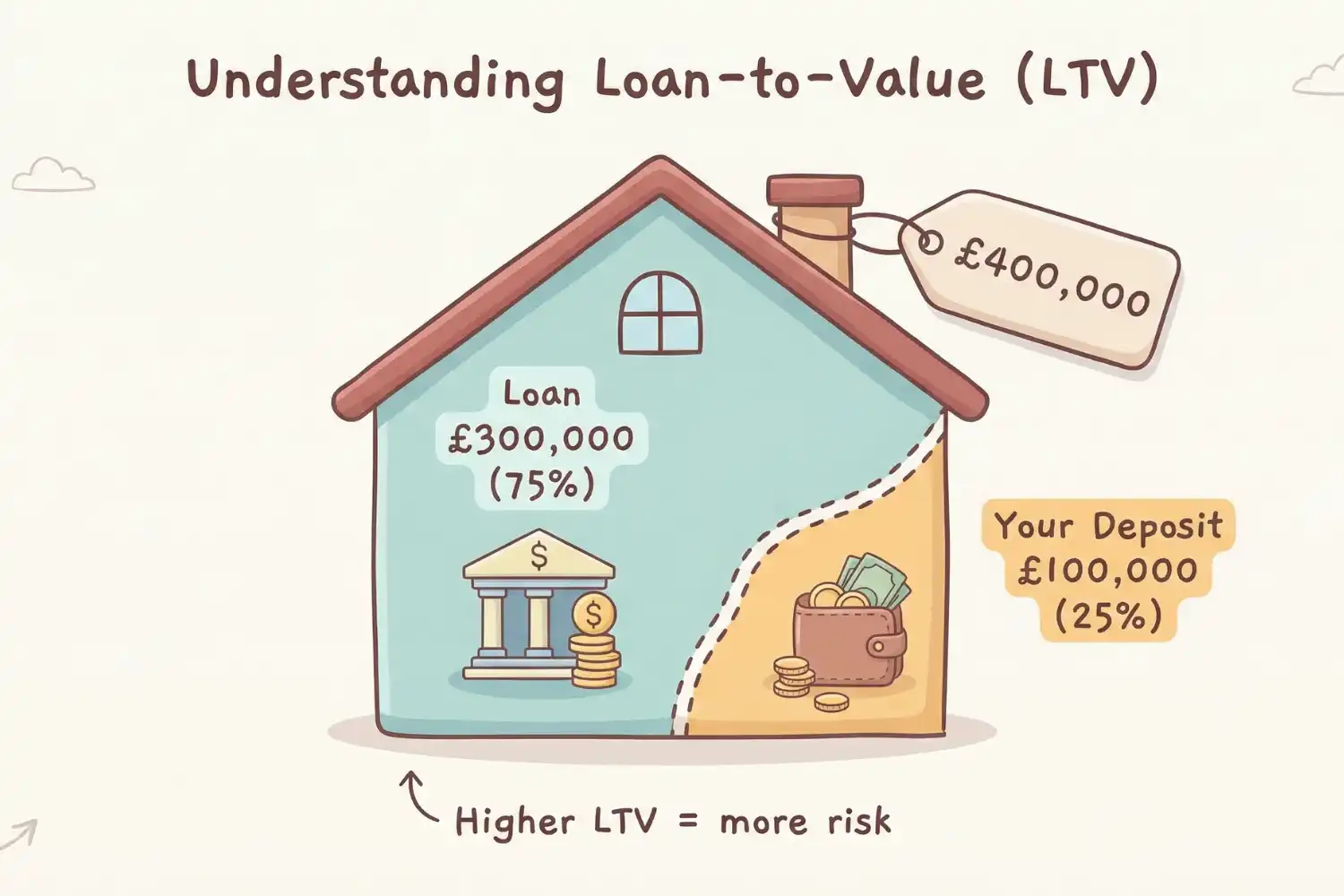

LTV stands for loan-to-value. It is the amount you are borrowing expressed as a percentage of the total value of the security you are offering. For example, if you want to borrow £300,000 against a property worth £400,000, that is 75% LTV. The remaining 25% — £100,000 — is the equity or deposit you need to provide.

The reason lenders focus so heavily on LTV is that it determines their level of risk. If a borrower defaults and the lender needs to recover funds by selling the security property, a lower LTV gives them far more room to absorb sale costs, market fluctuations, and legal fees before taking a loss. A higher LTV means the lender is more exposed, which is why higher LTV bridging loans attract higher interest rates and are harder to obtain.

For most bridging transactions, the relationship between bridging loan LTV and the deposit you need is simple: the lower the LTV, the less you need to contribute — and the cheaper and more accessible the loan becomes.

How much deposit do you typically need for a bridging loan?

The standard deposit for a bridging loan sits at around 25%–30% for residential property transactions, reflecting the typical maximum LTV of 70%–75% that most mainstream bridging lenders work to. For commercial or more complex transactions, the required deposit is usually higher.

The following table gives a general overview of minimum deposit expectations by loan type:

- Residential bridging loan: minimum deposit of around 25% (up to 75% LTV)

- Commercial bridging loan: minimum deposit of 30%–40% (60%–70% LTV), reflecting the lower liquidity and higher risk of commercial assets

- Second charge bridging loan: minimum 35%–40% equity required across the combined charges, as the lender sits behind an existing mortgage

- Heavy refurbishment or development: lenders often require higher deposits of 35%–50% where the project carries more execution risk

These are starting points rather than fixed rules. Some specialist lenders will go to 80% LTV — or even higher in exceptional circumstances — but this usually comes at a significantly higher interest rate and often requires additional security or a very strong exit strategy. Understanding these ranges is the first step to knowing whether a bridging loan is viable for your specific transaction.

If you are not yet sure whether bridging finance is the right tool for your situation, the guide to who bridging loans are best for covers the most common scenarios where bridging makes practical sense.

Does the deposit have to be cash?

This is one of the most important distinctions between bridging finance and a standard mortgage. When most people hear “deposit,” they think of cash savings. With a deposit for a bridging loan, the picture is quite different.

Bridging lenders are primarily focused on the quality and value of the security provided — not on whether it consists of cash. In practice, the most common forms of “deposit” used in bridging transactions include:

Equity in another property

If you already own a property — a family home, a buy-to-let, or another investment — the equity in that asset can be used as additional security to support your bridging loan. By adding this property to the security pool, you increase the total collateral value and reduce the effective bridging loan LTV, which may enable you to borrow more or secure a better rate.

For example, suppose you want to purchase a property for £500,000 and the lender offers 75% LTV. Normally, you would need £125,000 in cash as a deposit. But if you have a second property worth £300,000 with a £100,000 mortgage, the £200,000 equity in that property could be offered as additional security — potentially reducing or eliminating the need for a cash deposit entirely.

The property being purchased (for below-market-value deals)

If you are buying a property significantly below its open market value — a common scenario in auction purchases, distressed sales, or off-market deals — the gap between the purchase price and the true market value can effectively act as built-in equity. Some lenders will lend against the open market value rather than the purchase price, which means the deposit requirement relative to what you are paying can be substantially lower.

Multiple properties as cross-security

Where a single property does not provide enough security to hit the required LTV, lenders may accept multiple properties as combined collateral. This cross-charging approach pools the value of all the assets to calculate a blended LTV across the whole portfolio. It is a common technique among experienced property developers and investors managing a larger number of assets.

Not sure how much deposit you need for a bridging loan?

Most bridging loans require 25%–40% equity, but this does not always have to be cash. Property equity and additional security can reduce what you need to put in. Get expert advice

What factors affect your bridging loan deposit requirements?

Several variables influence how much deposit a lender will require for any given transaction. Understanding these factors helps you assess your position before approaching lenders, and can give you tools to potentially negotiate better terms.

Strength of the exit strategy

The exit strategy — the plan by which you will repay the bridging loan — is arguably the most important factor in the entire bridging loan assessment. A lender who is confident you can repay on time is more willing to extend a higher LTV, which means a lower deposit for a bridging loan. A clear, credible exit backed by evidence (a sale agreement, an agreement in principle for a remortgage, a confirmed development timeline) will generally attract better terms than a vague or aspirational plan.

Property type and condition

Standard residential property in good condition is the most favoured security for bridging lenders. It is easier to value, easier to sell if things go wrong, and there is a well-established market for it. Commercial property, unusual assets, and buildings in poor condition are seen as harder to liquidate, which pushes lenders toward lower LTV offers and higher bridging loan deposit requirements.

Borrower experience and credit profile

Bridging lenders place less weight on personal credit history than standard mortgage lenders, because the loan is secured against an asset rather than primarily assessed on income and affordability. However, credit history and the borrower’s experience are still considered — particularly when the LTV is at the higher end of the range. An experienced developer with a clean track record may access higher LTV deals than a first-time borrower with the same security.

First charge vs second charge

A first charge bridging loan — where there is no other secured debt on the property — offers the lender the strongest protection. First charge loans therefore tend to have more competitive LTV options. A second charge loan, where an existing mortgage already sits on the property, carries more risk because the bridging lender’s claim ranks behind the mortgage lender’s in the event of default. This additional risk typically means higher bridging loan deposit requirements for second charge arrangements.

Can you get a bridging loan with no deposit?

In theory, it is possible — but it requires a very specific set of circumstances. A bridging loan with no cash deposit is only viable if sufficient equity can be provided through other means to bring the LTV down to a level the lender is comfortable with. This might mean:

- Offering multiple properties as security so that the combined equity covers the full loan amount

- Purchasing significantly below market value, such that the discount itself provides the required equity buffer

- Using mezzanine finance — a second layer of lending that sits behind the first charge — to fill the gap between the senior loan and the purchase price

However, you cannot use one bridging loan to fund the deposit on another bridging loan. Lenders will check the source of the deposit or equity very carefully, and circular funding arrangements of this kind will not be accepted.

For the vast majority of borrowers, some form of genuine equity or security — whether in cash or property — will always be required. A 100% LTV bridging loan with no security whatsoever is not something mainstream lenders offer.

What else should you budget for alongside the deposit?

The deposit or equity you put in is only one part of the total cost of a bridging transaction. There are several additional costs to factor into your planning before you commit, as these can be significant and are often non-negotiable.

Arrangement fees are typically charged by the lender at 1%–2% of the loan amount. These can usually be added to the loan rather than paid upfront, but they do increase the overall borrowing and therefore the amount of interest accrued.

Valuation fees cover the independent valuation of the security property, which most lenders require before issuing a formal offer. These vary depending on the property type, value, and complexity of the case.

Legal fees are an important and sometimes underestimated cost in bridging transactions. You will typically need to pay your own solicitor’s fees as well as the lender’s legal costs. For more detail on what to budget for on this side of the transaction, the breakdown of legal fees involved in a bridging loan gives a clear overview of what to expect and why specialist conveyancing support matters.

Interest is charged monthly and can be structured in three ways: rolled up into the loan and repaid at redemption, retained upfront for the agreed term, or serviced monthly if you prefer to pay as you go. The method you choose will affect both the gross loan amount and your cash flow during the term.

Regulated vs unregulated bridging: does it affect the deposit?

Whether your bridging loan is regulated or unregulated can affect the deposit and LTV terms you are offered. A regulated bridging loan is one secured on a property where you or a close family member currently lives or intends to live. These loans fall under the oversight of the Financial Conduct Authority (FCA) and come with additional consumer protections. Regulated loans tend to be slightly more conservative in their LTV offers, reflecting the heightened duty of care toward borrowers. An unregulated bridging loan covers investment or commercial property — buy-to-let portfolios, development sites, commercial premises, and assets held through limited companies. Lenders in this space often have more flexibility on LTV and bridging loan deposit requirements, and some will consider higher LTV deals for experienced borrowers with strong security profiles. For a broader grounding in how these products work and which type is likely to apply to your situation, the full explanation of bridging loans for UK investors covers the key distinctions in straightforward terms. The FCA’s consumer guidance on mortgages and secured lending also provides useful background on your rights as a regulated borrower.Summary: what you need to know about bridging loan deposits

To bring together the key points:

- The typical deposit for a bridging loan is 25%–40% of the property’s value, depending on the loan type and risk profile of the transaction.

- Most mainstream lenders work to a maximum bridging loan LTV of 70%–75% for residential property and 60%–70% for commercial assets.

- The deposit does not need to be cash. Equity in another property, cross-security arrangements, or below-market-value purchases can all reduce or replace the need for cash.

- Your exit strategy, property type, and borrower profile all influence the LTV and bridging loan deposit requirements on offer.

- 100% LTV bridging with no security is not generally available — some form of genuine equity is always required.

- Always budget for additional costs including arrangement fees, valuation, legal fees, and interest, as these can add significantly to the overall cost of borrowing.

If you are planning a bridging transaction and want to understand the full picture — including the legal side of the process — our team is here to help. We work with borrowers and their brokers across a range of bridging scenarios, from simple chain-break bridges to complex development transactions. If you would like to discuss your situation and understand what will be involved from a legal perspective, get in touch with our team.

Need help understanding bridging loan deposit requirements?

The deposit for a bridging loan depends on loan-to-value, property type, and the strength of your exit strategy. Many lenders offer up to 70%–75% LTV, meaning you typically need 25%–30% equity — although this can vary for more complex transactions.

Our specialist solicitors work alongside lenders and brokers to ensure your bridging finance is structured correctly and completes smoothly.