When you start researching bridging finance, you will quickly encounter the distinction between an open bridging loan vs closed bridging loan — and understanding the difference matters before you apply. The two types of bridging loan are structured around a single core question: do you know exactly when and how you will repay the loan?

That question shapes everything else: the interest rate you are offered, how straightforward the approval process is, the penalties you face if things do not go to plan, and whether a particular bridging loan exit strategy is even viable. This guide sets out precisely how open and closed bridging loans differ, what each one is designed for, and how to decide which type of short-term property finance is right for your situation.

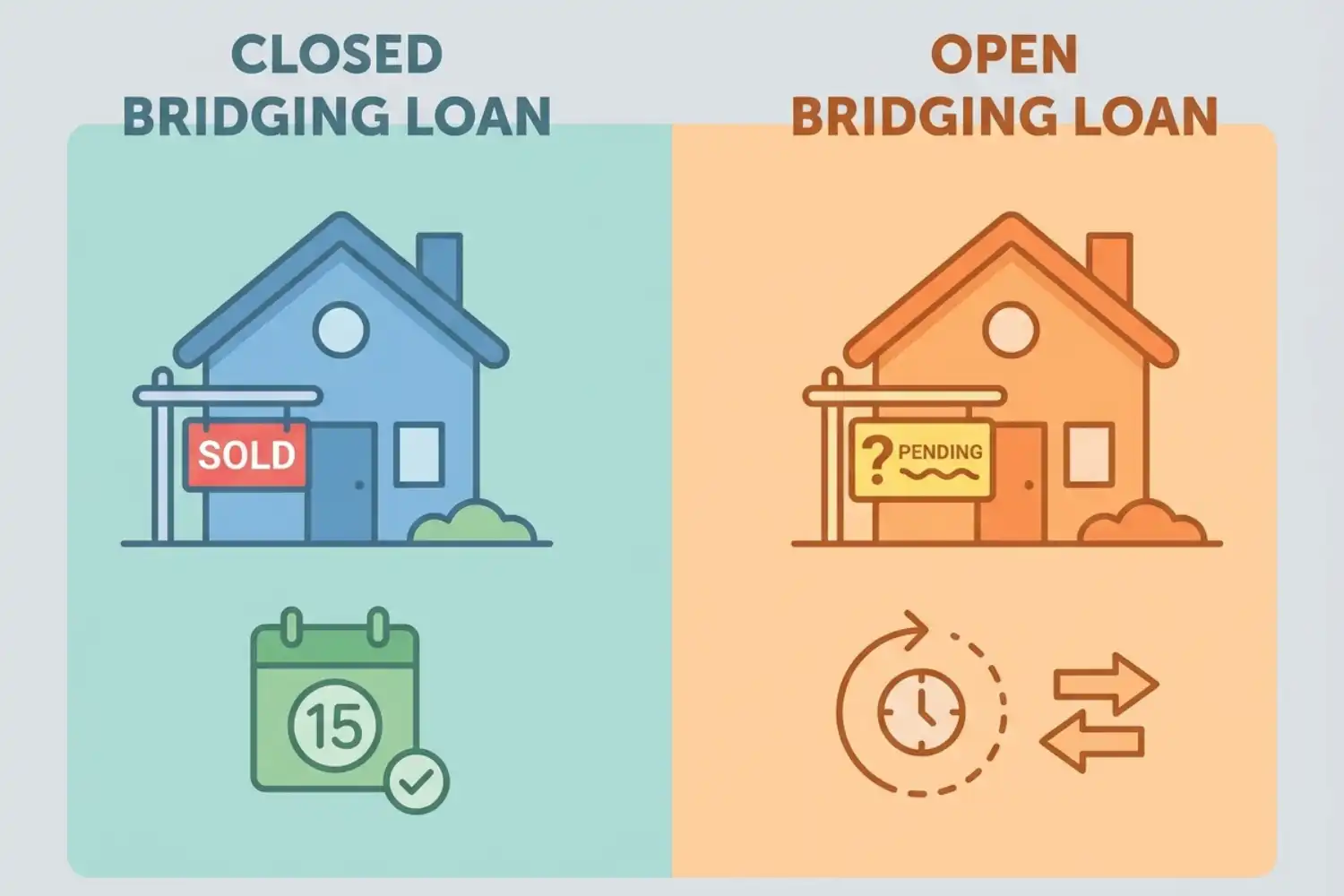

What is a closed bridging loan?

A closed bridging loan is a short-term loan with a fixed repayment date agreed at the point of application. The defining feature is certainty: both the borrower and the lender know precisely when the loan will be repaid, because the bridging loan exit strategy has already been confirmed and can be evidenced.

The most common example is a buyer who has exchanged contracts on the sale of their existing property. Exchange of contracts is legally binding — the completion date is set, and the sale proceeds will land on a known date. That certainty allows the lender to structure the loan around a fixed repayment schedule, which in turn reduces the risk they are carrying.

Other situations where a closed bridging loan is typically appropriate include:

- A confirmed mortgage offer with a drawdown date already agreed with the lender

- A property development project where the sale or refinancing of the completed asset is contractually agreed

- An inheritance or other receipt of funds where the date of payment is legally certain

- A business transaction where funds are due from a confirmed contract by a specific date

Because the lender’s risk is significantly lower on a closed bridging loan vs open bridging loan, the interest rates are generally more competitive and approval is more straightforward. If you can evidence your exit strategy, a closed loan is almost always the preferable option.

What is an open bridging loan?

An open bridging loan has no fixed repayment date. The borrower has a clear intention to repay — typically through the sale of a property or the completion of a refinancing — but the precise date cannot yet be confirmed. The bridging loan exit strategy exists, but it has not crystallised into a guaranteed timeline.

As a form of short-term property finance, open bridging loans are widely used in situations where the repayment source is identifiable but the timing is uncertain. Common scenarios include:

- Buying a property at auction before the existing property has been marketed or sold

- Purchasing a new home while the current property is on the market but has not yet found a buyer

- Funding a development project where planning permission is pending or the completion date is subject to construction timelines

- Acquiring a property quickly to take advantage of a time-sensitive opportunity before longer-term finance is arranged

The absence of a fixed date is the key distinction in the open bridging loan vs closed bridging loan comparison. Lenders will typically allow up to twelve months for repayment of an open bridging loan, though some specialist lenders offer terms of up to twenty-four months in specific circumstances. The flexibility comes at a cost: interest rates are higher, reflecting the greater uncertainty the lender is carrying.

Open bridging loan vs closed bridging loan: side-by-side comparison

The table below summarises the key differences at a glance.

| Closed bridging loan | Open bridging loan | |

|---|---|---|

| Repayment date | Fixed — agreed at outset | Flexible — no set date, usually within 12 months |

| Exit strategy | Confirmed and evidenced (e.g. exchange of contracts) | Planned but not yet confirmed |

| Interest rate | Lower — lender carries less risk | Higher — lender carries more risk |

| Ease of approval | Easier — lenders prefer certainty | Harder — requires strong credit and clear rationale |

| Missed date penalty | Yes — significant penalties if repayment is missed | No fixed date to miss, but interest compounds |

| Best suited to | Property chain completion, confirmed sale proceeds, mortgage drawdown | Auction purchases before sale, uncertain sale timelines, development projects |

Why your bridging loan exit strategy is the deciding factor

The difference between an open bridging loan vs closed bridging loan ultimately comes down to one thing: the status of your exit strategy. The exit strategy is the mechanism through which you will repay the loan — and whether that mechanism is confirmed, contractually certain, or still contingent determines which type of loan you will be offered and on what terms.

Lenders assess exit strategies carefully, regardless of whether the loan is open or closed. For a closed loan, they will typically require documentary evidence of the confirmed exit — exchange of contracts, a formal mortgage offer, or a signed completion statement. For an open loan, they will want to understand the proposed exit in detail even though the date is not fixed: which property is being sold, what evidence of marketability exists, what the realistic timeline looks like, and what the contingency plan is if the primary exit takes longer than anticipated.

A poorly evidenced exit strategy — open or closed — is one of the most common reasons short-term property finance applications are declined or offered on unfavourable terms. Lenders are not simply assessing the value of the security property; they are assessing the credibility and reliability of the repayment plan. The stronger and more detailed the exit strategy, the better the terms you are likely to be offered, and the smoother the legal process will be.

Interest rates and costs: understanding the difference

Interest rates on bridging finance are expressed monthly rather than annually, because bridging loans are short-term instruments. On a closed bridging loan, monthly rates are generally lower — reflecting the certainty the lender has about repayment timing. On an open bridging loan, rates are higher to compensate for the open-ended risk.

The practical implication of this is significant. Even a difference of 0.2% per month compounds meaningfully over the life of a loan. On a £300,000 bridging loan held for nine months, the difference between a competitive closed rate and a typical open rate could amount to several thousand pounds in additional interest. This is one of the strongest practical arguments for choosing a closed bridging loan whenever your exit strategy allows for it.

In addition to interest, short-term property finance typically involves arrangement fees (usually 1–2% of the loan amount), valuation fees, and legal costs at both the lender’s and borrower’s end. These costs apply to both open and closed loans. Some lenders offer rolled-up interest — where interest is added to the loan balance rather than paid monthly — which can ease cashflow during the loan term but increases the total amount repayable.

Not sure whether you need an open or closed bridging loan?

The key difference is your exit strategy. If your repayment date is fixed, a closed loan may offer lower rates — but if timing is uncertain, an open loan provides flexibility at a higher cost. Get expert guidance

Risks to understand before you borrow

Missing the repayment date on a closed bridging loan

Closed bridging loans carry a specific risk that open bridging loans do not: the consequences of missing the fixed repayment date. If completion of your property sale is delayed — a buyer pulls out, a chain collapses, or legal issues arise at the last moment — and you cannot repay on the agreed date, the penalties can be substantial. The loan may revert to a default rate, which is significantly higher than the contracted rate, and the lender has the right to enforce their security against the property.

This is why it is essential to build realistic contingency into your timeline when taking out a closed bridging loan. If your exit depends on a property sale completing, ensure the loan term extends beyond the expected completion date to give you a buffer. A closed bridging loan vs open bridging loan is almost always cheaper — but only if your exit strategy is as certain as it appears.

Compounding interest on open bridging loans

Open bridging loans carry a different but equally serious risk: interest that compounds if the exit takes longer than planned. Because there is no fixed repayment date, it is easy to underestimate how much the loan will cost if the sale of the security property is delayed by several months. As a form of short-term property finance, bridging loans are not designed to be held for extended periods — the monthly interest rate makes prolonged borrowing expensive. Always model the cost of the loan at your expected timeline and at a pessimistic timeline before committing.

Lender enforcement

Both open and closed bridging loans are secured against property. If you are unable to repay — whether because your bridging loan exit strategy has failed, a sale has fallen through, or a remortgage has not completed — the lender can enforce their security charge and take possession. This applies to residential and commercial property alike, and it applies to first and second charge loans. Understanding this risk clearly before you borrow is essential.

Which should you choose: open or closed bridging loan?

The decision between an open bridging loan vs closed bridging loan is rarely a matter of preference — it is determined by the facts of your situation.

- Choose a closed bridging loan if your exit strategy is confirmed and evidenced. If you have exchanged contracts on a sale, received a formal mortgage offer with a drawdown date, or have legally confirmed funds arriving on a known date, a closed loan will give you lower rates and a smoother approval process.

- Choose an open bridging loan if your exit is clearly identifiable but the timing is not yet certain. If you are buying before selling, bidding at auction, or funding a development with a flexible completion timeline, an open loan gives you the flexibility you need — at a higher cost that must be factored into your planning.

In either case, the legal framework around short-term property finance — the loan documentation, security charges, lender requirements, and exit mechanics — is more complex than many borrowers anticipate. Having the right legal advice from a solicitor experienced in bridging transactions protects you at every stage: from reviewing the loan agreement and the conditions attached to it, through to ensuring the security is properly registered and your exit completes cleanly.

Get clear legal advice before you commit to a bridging loan

Whether you are weighing up an open bridging loan vs closed bridging loan, assessing the strength of your bridging loan exit strategy, or navigating the legal requirements of a bridging transaction under time pressure, specialist legal support makes the process faster and significantly reduces the risk of costly complications. At Bridging Loan Lawyers, we work exclusively in this area of property finance law — advising borrowers on loan documentation, security arrangements, title issues, and exit mechanics across residential and commercial transactions throughout England and Wales. Speak to our team directly to discuss your situation and find out how we can help you move forward with confidence.

Need advice on choosing the right bridging loan?

Whether you need an open or closed bridging loan depends on how certain your exit strategy is. The right structure affects your interest rate, risk, and ability to complete on time — and getting it wrong can be costly. Our specialist solicitors help you review loan terms, assess your exit strategy, and ensure your bridging finance is structured correctly from the outset.