The bridging loan application process can feel unclear once you have submitted your initial enquiry. You have handed over your documents and are waiting — but you do not know what is happening, how long each stage takes, or what could go wrong. That uncertainty is one of the most stressful parts of taking out a bridging loan, particularly for first-time borrowers.

The good news is that the process follows a predictable sequence. Once you understand what each stage involves and why it takes the time it does, the waiting becomes far less anxious. This guide walks you through every step in plain terms, from the decision in principle right through to funds in your account.

Most applications complete within five to 14 working days. More complex cases — unusual property types, leasehold complications, or a less conventional exit strategy — may take up to four weeks. Knowing where you are in the timeline at any given moment puts you firmly in control.

The bridging loan application process: an overview

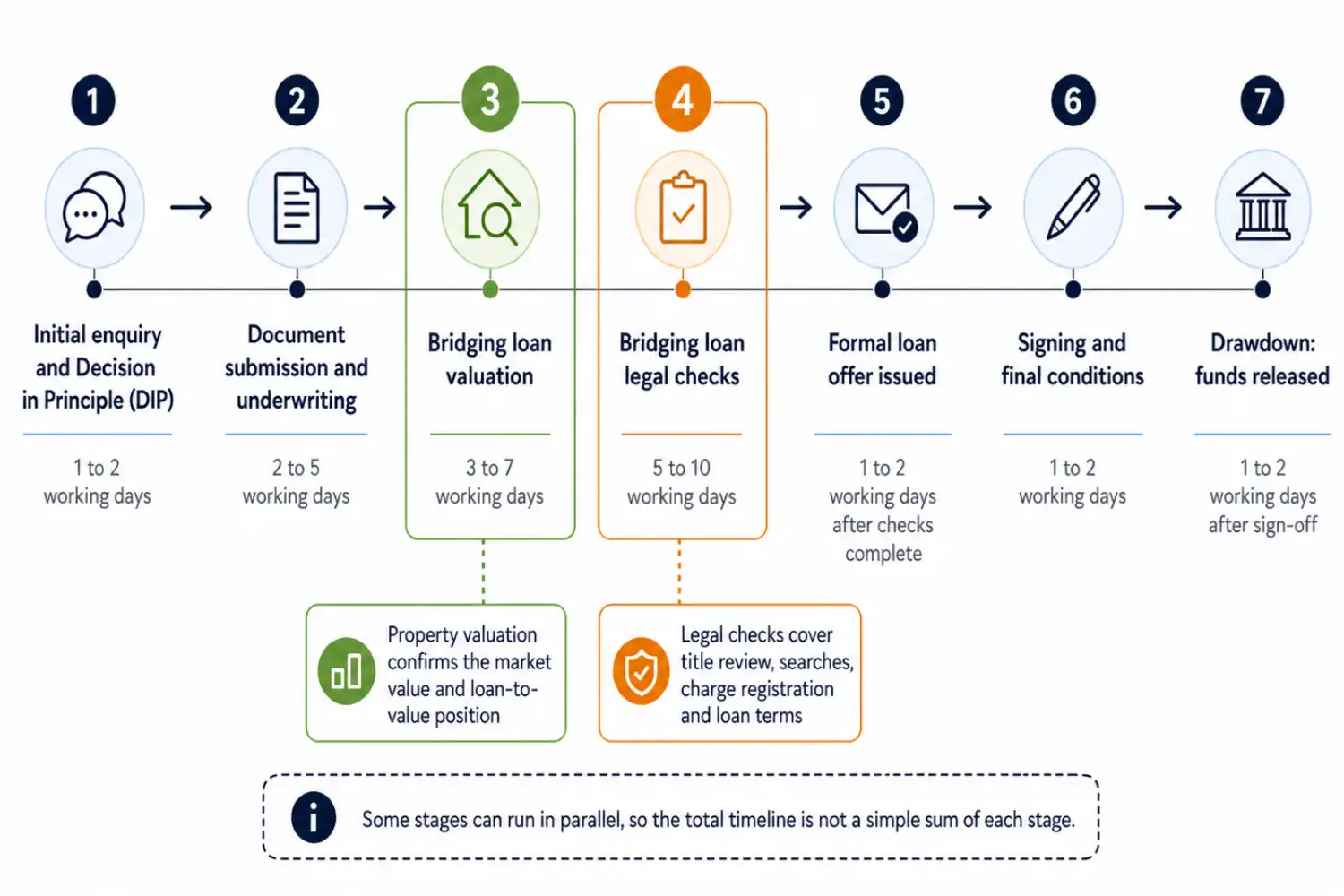

Before going stage by stage, it helps to see the full sequence at a glance. The bridging loan application process moves through seven distinct steps, each dependent on the one before it.

- Initial enquiry and Decision in Principle (DIP) — 1 to 2 working days

- Document submission and underwriting — 2 to 5 working days

- Bridging loan valuation — 3 to 7 working days

- Bridging loan legal checks — 5 to 10 working days

- Formal loan offer issued — 1 to 2 working days after checks complete

- Signing and final conditions — 1 to 2 working days

- Drawdown: funds released — 1 to 2 working days after sign-off

The total timeline is not simply these figures added together. Several stages run in parallel, and your preparation has a significant influence on speed. A borrower who has documents ready from day one will complete faster than one who gathers paperwork as each request arrives.

Stage 1: your initial enquiry and Decision in Principle

The process begins before any formal application is submitted. When you first contact a lender or broker with your requirements, they will assess whether your case is viable — typically within a few hours to 24 hours for straightforward situations.

This initial assessment covers the key questions: what is the property being used as security, what is the loan amount you need relative to the property value, what is your exit strategy, and are there any credit or legal issues the lender should know about upfront? The lender is not conducting detailed due diligence at this stage — they are simply checking whether your case is broadly within their lending criteria.

If the lender is satisfied, they will issue a Decision in Principle (DIP) — sometimes called an Agreement in Principle or Indicative Terms. This is a conditional indication that they are likely to lend, subject to full underwriting. A DIP does not guarantee the loan, but it does mean you are not wasting time on a lender who will not be able to help.

Receiving a DIP typically takes one to two working days. Some specialist lenders can issue same-day DIPs for straightforward cases. The quality of information you provide at this stage affects how quickly and confidently the lender can respond.

Stage 2: document submission and formal underwriting

Once you have accepted the DIP and chosen to proceed, the formal underwriting begins. This is where the bridging loan application process moves from conditional to substantive. The lender’s underwriter reviews your application in full and assesses the risk of lending.

You will be asked to provide your supporting documentation at this stage. Having everything ready in advance is the single most effective way to compress the timeline. Delays at the underwriting stage almost always trace back to missing or incomplete documents.

The documents typically required include proof of identity, proof of address, evidence of the exit strategy (such as a property listed for sale, or a mortgage in principle for a refinance), details of the security property, and — for larger or more complex loans — financial background on the borrower. Our full guide to what documents you need for a bridging loan covers every category in detail so you can prepare a complete pack before submitting.

Formal underwriting typically takes two to five working days, but this can be shorter if your documents are clean and complete from the outset.

Worried your bridging loan timeline could slip?

Approval is only one part of the process. Your valuation, property title, searches, lender conditions, signed documents, and exit strategy all affect how quickly funds can be released. Getting a solicitor involved early can help identify legal issues before they delay the formal offer or drawdown. Get legal guidance during your bridging loan application

Stage 3: the bridging loan valuation

The bridging loan valuation is one of the two stages that most commonly causes delays, and it is the one borrowers tend to have least control over. Understanding it clearly can help you manage expectations — and take one action that meaningfully speeds things up.

Once the underwriter is satisfied with your documents, the lender will instruct a surveyor to assess the property being offered as security. The purpose of the bridging loan valuation is to confirm the current market value of the property, which determines both the loan amount and the loan-to-value ratio the lender is prepared to offer.

Most lenders instruct RICS-qualified surveyors to carry out valuations. The Royal Institution of Chartered Surveyors (RICS) standards for property valuation are the benchmark used across the UK bridging and mortgage market, and lenders will only accept reports from qualified, independent surveyors.

When bridging loan approval speed matters most

Not every bridging loan is a rush job, but some situations make every day count. The clearest example is an auction purchase, where buyers typically have 28 days from the fall of the hammer to complete, and losing the deposit is a real risk.

If that is your situation, our guide on bridging loans for auction properties explains exactly how to align the legal work with that 28-day window so nothing slips.

Other common scenarios where the bridging loan timeline becomes mission-critical include:

- A property chain on the verge of breaking, where a delayed completion loses the onward purchase

- Investors who need to secure a discounted property before the seller accepts another offer

- Short-notice refurbishment or conversion work with contractor start dates already booked

- Business owners using a bridging loan to complete a commercial purchase before a lease deadline

In each of these cases, the bridging loan process has to align with an external deadline that simply will not move. That makes upfront preparation, rather than last-minute chasing, the real key to getting approval in time.

Types of bridging loan valuation

There are three main approaches a lender may use for the bridging loan valuation, and the type chosen depends on the lender, the property, and the complexity of the transaction.

- Desktop valuation: the surveyor assesses the property using available data — Land Registry records, comparable sales, and local market information — without a physical visit. This is the fastest option, often completed within one to two working days, and is used for standard properties in well-documented locations where there is strong comparable evidence.

- Drive-by or kerb-side valuation: the surveyor visits the property but only assesses the exterior, relying on internal details from the application. Faster than a full inspection and typically completed within two to four working days.

- Full physical inspection: the most thorough option, involving access to the interior of the property. Required for unusual properties, development projects, or higher-value loans where the lender needs complete confidence in the security. Typically takes five to seven working days to arrange, inspect, and report.

The one thing you can do to speed up the bridging loan valuation is to ensure the property is accessible and that you or your agent can facilitate access at short notice. Delays in getting surveyors into a property are a common cause of unnecessary wait time.

Stage 4: bridging loan legal checks — what your solicitor does

The bridging loan legal checks stage runs in parallel with — and sometimes beyond — the valuation process. It is typically the longest single stage in the application, and it is the one where the involvement of an experienced solicitor makes the most measurable difference to speed and outcome.

The lender will instruct their own solicitor to handle the legal work. You are also required to have your own independent legal representation — your solicitor acts exclusively in your interests and ensures you understand what you are agreeing to. In some bridging transactions, particularly smaller residential ones, the same firm may act for both parties (known as dual representation), but this is not universal.

The bridging loan legal checks cover several distinct areas:

- Title investigation: your solicitor reviews the Land Registry title to ensure the property is owned by who claims to own it, that there are no unexpected restrictions or third-party interests, and that the legal description matches what is being offered as security

- Property searches: standard searches are submitted — local authority, drainage and water, environmental, and in some areas coal mining or flood risk searches. These reveal planning issues, restrictions, or environmental risks that could affect the value or use of the property

- Charge registration: the lender’s charge over the property is registered at Land Registry once all checks are satisfied, giving the lender priority security over the asset

- Loan agreement review: your solicitor reviews the full loan agreement, including interest rate, fees, repayment date, default provisions, and any special conditions, ensuring the terms are what was agreed and that there are no onerous clauses buried in the documentation

Our guide to whether you need a solicitor for a bridging loan explains why independent legal advice is not just required by lenders — it is one of the most important protections you have as a borrower. Leasehold properties, properties with complex titles, or those with planning history almost always require more thorough legal work, which extends this stage. The best way to avoid delays here is to instruct a solicitor who has specific experience in bridging transactions — not a general conveyancer who treats it like a standard purchase.

Most bridging loan legal checks complete within five to ten working days for standard freehold residential properties. More complex cases can take longer, particularly where searches reveal issues that need to be resolved or where title defects require remedial action.

Stage 5: the formal loan offer

Once the bridging loan valuation report has been received and the bridging loan legal checks are satisfied to the lender’s standard, the lender issues the formal loan offer. This is a binding document setting out the terms on which the lender is willing to proceed: the loan amount, the interest rate, the term, the fees, the repayment date, and any conditions that must be met before drawdown.

Read this document carefully. It supersedes everything discussed verbally and in correspondence. If anything differs from what was agreed at DIP stage — a lower loan amount because the valuation came in below expectation, additional conditions, a higher rate than anticipated — this is the point to address it. Your solicitor should review the offer alongside you and flag anything that warrants clarification or negotiation before you accept.

The loan offer is typically issued within one to two working days of the lender receiving a satisfactory valuation and clean legal report. How quickly it arrives depends on how smoothly both the valuation and legal stages concluded.

Understanding how long each of these stages takes in practice — and the variables that affect the timeline — is covered in more depth in our guide to how long bridging loan approval takes in the UK.

Stage 6: signing and satisfying final conditions

After accepting the formal offer, you and your solicitor will execute the loan documentation. This involves signing the loan agreement and the legal charge — the document that gives the lender their security over the property.

Most loan offers include a set of conditions that must be confirmed before funds can be released. These commonly include evidence of buildings insurance on the secured property, confirmation that any earlier charges have been redeemed or prioritised, and certification that there are no changes to the circumstances stated in the application.

This stage is usually straightforward where the application has been well-prepared throughout. It typically takes one to two working days. Delays at this stage are rare but can occur if a condition from the offer proves more complex to satisfy than anticipated — for example, if a redemption figure on an existing charge takes longer than expected to receive.

Stage 7: drawdown — when the funds are released

Drawdown is the moment the lender releases the funds to your solicitor’s client account. It is the final step in the bridging loan application process, and it is the point at which your loan formally begins — meaning the clock on your repayment term starts from this date.

In practice, drawdown occurs on an agreed completion date. Your solicitor and the lender’s solicitor confirm that all conditions are met, that searches are clear, and that the charge documentation is in order. The lender then authorises the transfer of funds. Your solicitor receives the money in their client account and uses it to complete the transaction — whether that is paying the purchase price of a property, redeeming an existing charge, or releasing cash to you for another purpose.

The entire drawdown process, once all prior stages are complete, typically takes one to two working days. In urgent cases, same-day drawdown is possible where the legal and valuation work has been finalised in advance.

What happens after drawdown: repayment and your exit strategy

Once the funds are drawn, the loan is live. Interest accrues from the drawdown date, and you are working towards your repayment date. Your exit strategy — the plan you presented to the lender at application — is now the timeline you are working to.

Most bridging loans are repaid either by selling the secured property or by refinancing onto a standard mortgage. Some borrowers repay from other funds — inheritance, business proceeds, or a sale of a different asset. Whatever your exit route, do not leave it to the last few weeks of the term to act. If a property sale is your exit, it should ideally be underway — ideally with an accepted offer in place — before your loan reaches its final month.

If your exit is taking longer than expected, contact your lender or solicitor early. Lenders can often extend terms, though this typically involves additional fees. It is far better to request an extension when you still have time than to approach the repayment deadline already in difficulty.

Understanding the full picture of what can go wrong — and how to manage those risks — is equally important as understanding the application itself. Our guide to the risks of taking out a bridging loan covers the most common pressure points borrowers face during the loan term and how experienced legal support helps you navigate them.

The role of your solicitor throughout the bridging loan process

A specialist bridging loan solicitor is not just a formality required by the lender. Throughout the bridging loan application process, your solicitor is the person who reviews every document before you sign it, identifies problems in the title or legal structure before they cause delays, ensures the loan terms match what was agreed, and manages the mechanics of drawdown with the precision the lender requires.

For new borrowers in particular, having legal representation that communicates clearly at every stage — explaining what is happening, what is being reviewed, and what you need to do next — makes the process far less anxious. The confusion most borrowers feel after submitting an application comes from silence, not from complexity. A good solicitor removes that silence.

Bridging Loan Lawyers acts exclusively for borrowers. We do not act for lenders. That means every piece of advice we give is entirely focused on protecting your position — reviewing the terms before you commit, handling the bridging loan legal checks on your behalf, and ensuring the transaction completes as quickly and cleanly as possible. If you are at any stage of the bridging loan application process and want a clear, jargon-free conversation about where things stand, our team is here to help.

Need help keeping your bridging loan application on track?

The bridging loan application process can move quickly, but delays often happen during valuation, legal checks, title review, offer conditions, or final drawdown. A specialist bridging loan solicitor can review the lender’s requirements, handle the legal checks, explain the loan documents, and help keep your application moving towards completion without avoidable legal delays.