Getting your bridging loan documents ready before you apply can save you weeks of waiting. Lenders move quickly on bridging finance, but only once they have everything they need to assess your case properly.

Whether you’re buying at auction, plugging a gap in a property chain, or funding a refurbishment, having the right paperwork speeds up your bridging loan application considerably. This guide walks through exactly what you’ll need, from identification through to your exit strategy, so nothing catches you out.

Bridging finance can often complete in days rather than weeks, but only when your paperwork is in order from the very first enquiry. Lenders and solicitors can only move as fast as the slowest document in the pile, so it’s worth getting organised before you submit anything.

What documents do you need for a bridging loan application at a glance?

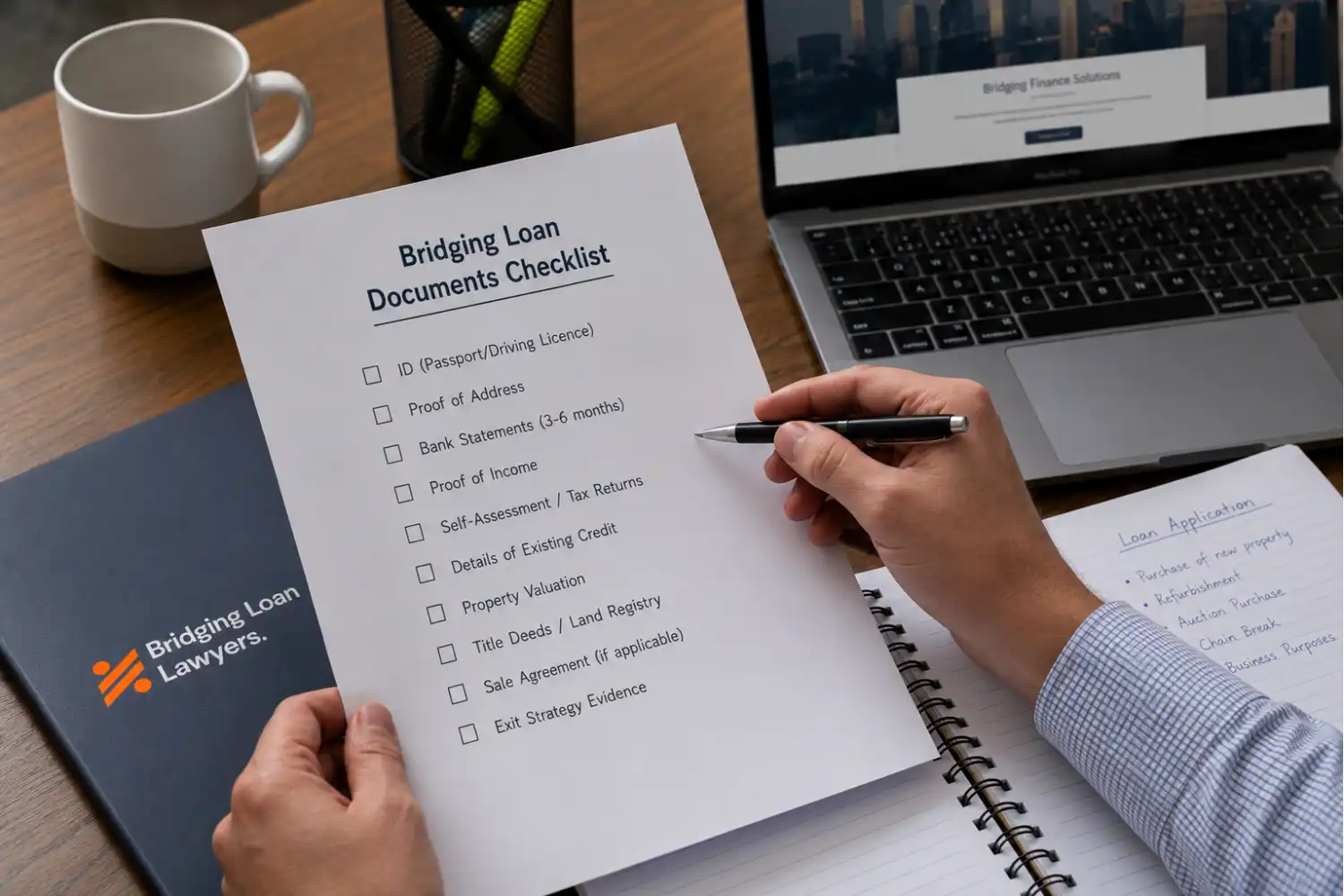

Every lender has slightly different requirements, but most bridging loan documents fall into four broad categories: identification, financial proof, property paperwork, and evidence of your exit strategy. Pulling these together early makes your bridging loan application far smoother.

At a glance, you’ll typically need:

- Proof of identity (passport or driving licence)

- Proof of address (recent utility bill or bank statement)

- Bank statements, usually covering the last three to six months

- An independent property valuation report

- Title deeds or proof of ownership

- Clear evidence of your exit strategy

Not every lender asks for all of these straight away. Many start with a simple decision in principle, then request your full bridging loan documents once your case looks viable.

A decision in principle is usually just a short form covering the loan amount, the term, and your repayment plan. It’s only once you move past this stage that the lender’s underwriters will ask for certified copies of everything listed above.

Proof of identity and address

What counts as valid ID and proof of address?

Lenders need to confirm you are who you say you are before they release any funds. This step is standard across every bridging loan application, regardless of which lender you approach.

Commonly accepted documents include:

- A valid passport, often the preferred option

- A full driving licence

- A recent utility bill (gas, electricity, water or phone)

- A bank or building society statement

- A council tax bill

Proof of address documents usually need to be dated within the last three months. If your name or address has changed recently, flag this early, as it can otherwise hold up your bridging loan documents during underwriting.

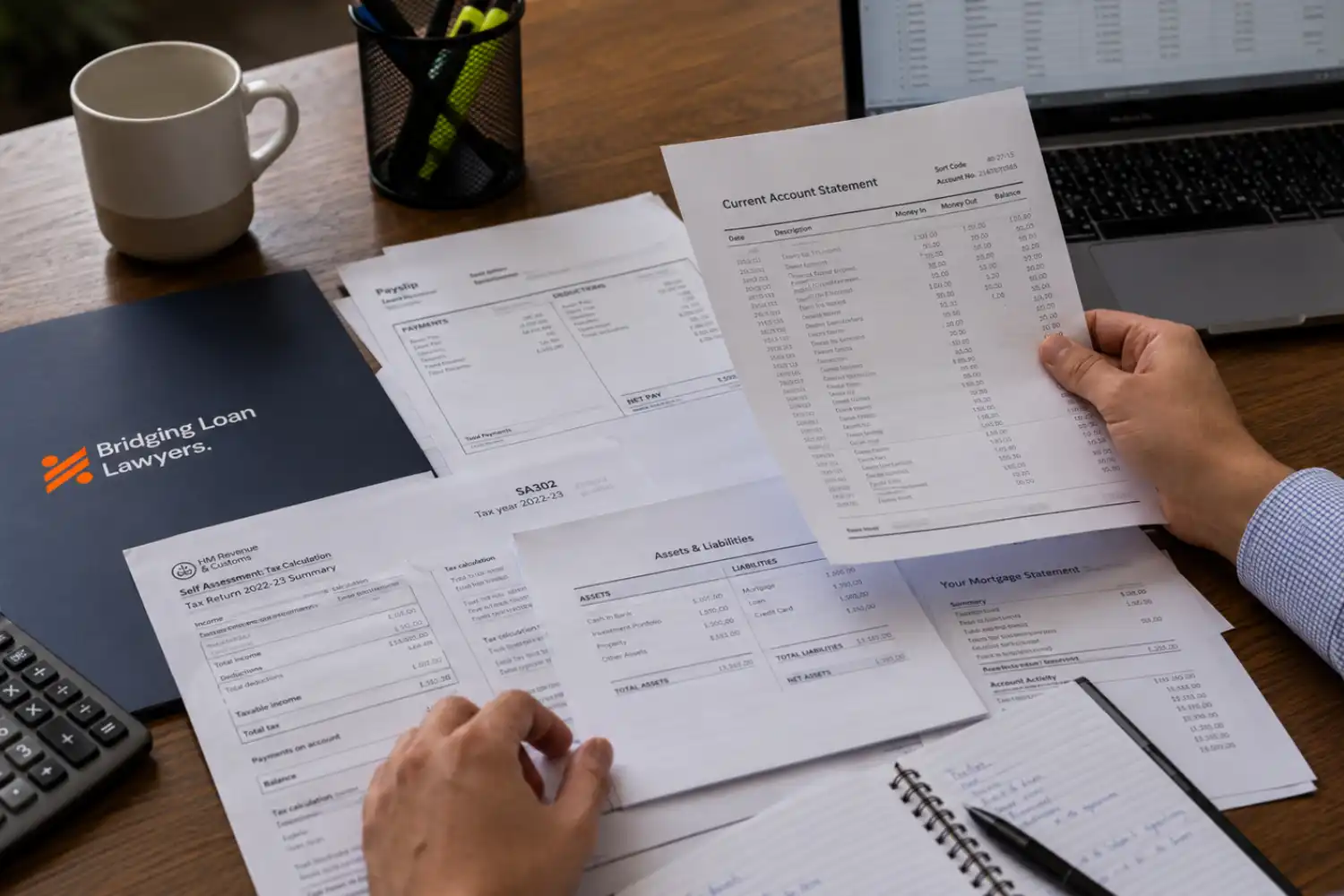

Financial documents lenders will ask for

Bridging loans are secured against property, so lenders focus less on income than they would for a standard mortgage. Even so, most still want reassurance that you can manage interest payments if your exit strategy takes longer than expected.

You should expect to provide some combination of the following:

- Bank statements covering the last three to six months

- Payslips or pension statements

- SA302 forms or tax return summaries if you’re self-employed

- A statement of your assets and liabilities

- Details of any existing loans or mortgages

If you’re self-employed or run a limited company, expect to provide a little more detail. Profit and loss accounts or an accountant’s reference often help your bridging loan application move along faster, since they give the lender extra confidence in your numbers.

This is also where lenders look at affordability for the interest payments themselves, rather than the whole loan. Even on a rolled-up or retained interest product, most lenders still want to see that you could cover the monthly cost if your exit strategy were ever delayed.

Property valuation and legal documents

Because your loan is secured against property, the lender will arrange an independent valuation report before releasing any funds. This determines the loan-to-value ratio and directly affects how much you can borrow. We’ve covered this in more detail in our guide to how a bridging loan valuation works.

You’ll also need legal documents proving you own, or are buying, the property used as security. These typically include the title deeds, a property sale agreement if you’re purchasing, and lease details if the property is leasehold.

Common legal documents include:

- Title deeds or the Land Registry entry

- A property sale agreement, if you’re buying

- A lease agreement, where the property is leasehold

- Evidence of any existing mortgage or charge

If you’d like to check who owns a property or confirm boundary details before you apply, you can search the Land Registry.

Not sure which bridging loan documents apply to your case?

Every bridging loan application is a little different, and the exact paperwork you need often depends on your exit strategy and whether more than one property is involved. Our team can talk you through exactly what to gather before you approach a lender, so book a free consultation whenever it suits you.

Proving your exit strategy

Lenders want to see a credible plan for repaying the loan, known as your exit strategy. This is one of the most closely scrutinised parts of any bridging loan application, because it tells the lender how and when they’ll get their money back.

If you’re selling a property, a marketing agreement or memorandum of sale will usually do. If you’re remortgaging instead, you’ll need a mortgage offer or an agreement in principle. Once the loan is eventually repaid, your solicitor will request a redemption statement to confirm the exact amount owed before the charge is removed.

There’s a third route too: repaying from business proceeds or other investments. In that case, lenders typically want evidence of the source, such as a signed contract, a maturing investment, or correspondence confirming funds are due within a realistic timeframe.

Why a bridging loan solicitor checks your paperwork

A bridging loan solicitor reviews your documents on behalf of the lender, checking for anything that could delay completion or put your security at risk. This includes confirming there are no hidden restrictions or unexpected charges against the property, something we explain further in why you need a bridging loan solicitor.

If you already have a mortgage or another loan secured against the property, your bridging loan solicitor may need to arrange a deed of postponement, so the new lender’s charge is correctly ranked alongside the existing one.

Extra documents if you’re using multiple properties or have a complex case

If your bridging loan is secured against more than one property, expect to provide separate valuation reports and title information for each one. Property investors and portfolio landlords should have this ready before approaching a lender, as it speeds up underwriting considerably.

Dealing with an inherited property or an estate? You may need extra evidence, such as a grant of probate, alongside your usual bridging loan documents. We’ve covered this in detail in our guide on using a bridging loan for probate property.

If you already have a mortgage on the property and you’re taking out a second charge bridging loan, you’ll also need written consent from your existing lender. Most will provide this once they understand the new loan won’t affect their own security.

How to avoid delays with your bridging loan documents

Most delays in a bridging loan application come down to missing or out-of-date paperwork rather than anything more complicated. A little preparation goes a long way.

- Check the lender’s exact document list before you apply

- Gather your ID, address proof and bank statements in advance

- Make sure your exit strategy evidence is current and specific

- Keep your property and legal documents together in one file

- Respond quickly if your bridging loan solicitor requests anything extra

Being organised from the outset is one of the biggest factors in how quickly your bridging loan completes, often making the difference between a smooth transaction and a frustrating one.

Ready to get your bridging loan application moving?

Pulling together the right bridging loan documents from the start makes the whole process faster and far less stressful. Our team can review your paperwork and flag anything missing before you submit your application, giving you one less thing to worry about.